2024 B.C. Budget: More Changes to B.C.’s Real Estate Landscape

On February 22, 2024, the government of British Columbia released its Budget and Fiscal Plan 2024/2025 - 2026/2027 (the “Budget”) outlining the province’s priorities for the coming fiscal year.[1] The Budget included several measures aimed at improving housing affordability in the province, including:

- the introduction of a new Home Flipping Tax;

- an expansion of the existing Property Transfer Tax (“PTT”) exemption amounts for first-time home buyers and purchasers of newly built housing; and

- additional funding for the BC Builds program.

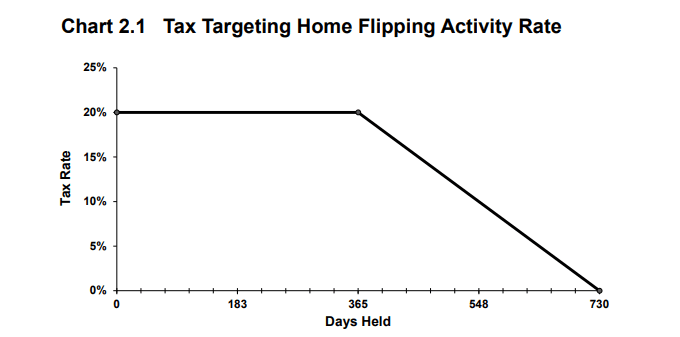

B.C. Home Flipping Tax

Effective as of January 1, 2025, the provincial government is introducing a new Home Flipping Tax on real estate sold in British Columbia.[2] This tax will target residential real estate sold within two years of the initial purchase, and apply to both residential properties and the assignment of purchase contracts for residential properties. The Budget states that tax exemptions will be available to people facing difficult life circumstances, including divorce, death, disability and more. Additionally, carve outs from the tax are expected for activities that increase the housing supply, though the Budget is unclear about what these carve outs might be. As shown in the chart below (extracted from the Budget), profits generated from house flipping will be taxed at a rate of 20% of such profits for the first year the property is owned and then the tax will phase out over the course of the second year.

Property Transfer Tax Exemptions – First Time Home Buyers, Newly Built Homes, and Rental Buildings

The Budget proposes to expand existing PTT exemptions for first time home buyers, newly built homes, and purpose-built rental buildings.[3] Previously, first time home buyers were not required to pay any PTT on the first $500,000 of the value of a home, provided that the home was not worth more than $500,000. Beginning April 1, 2024, the threshold for the PTT exemption will be extended to include homes with values of up to $835,000, such that additional first time home buyers will be exempt from paying PTT on the first $500,000 of the value of a home. PTT will, however, be payable for the portion of the value between $500,000 and $835,000. For amounts over $835,000, the exemption received for the initial $500,000 will get phased out. Then, for amounts over $860,000, there will be no PTT exemption and the tax will be payable on the entire amount.

Also beginning April 1, 2024, qualifying purchasers of newly built homes will receive a PTT exemption for the purchase of a principal residence valued at up to $1,100,000 (increased from $750,000). For amounts between $1,100,000 and $1,150,000, purchasers will receive a partial PTT exemption which will reduce, but not eliminate, the taxes owed. For amounts over $1,150,000, purchasers will be required to pay PTT.

For transactions that occur between January 1, 2025 and December 31, 2030, purchasers of qualifying purpose-built rental buildings will be exempt from the general property transfer tax. To qualify for the exemption, the residential portion of the building must be used for rental purposes and have at least four apartments. This policy, in conjunction with the federal government’s elimination of the 5% GST payment on newly built rental developments, will help reduce costs for rental housing projects and, in theory, incentivize the construction of additional rental buildings.

Speculation and Vacancy Tax Act

Minor changes were announced to the existing Speculation and Vacancy Tax Act.[4] Beginning January 1, 2024, persons who have leases registered in the Land Title Office will be responsible for paying this tax, rather than the owners of the property. This means that tenants with registered leases will have to make a declaration and be responsible for ensuring the property is occupied.

BC Builds Program

The Budget also outlines additional funding to be put towards the BC Builds program. BC Builds seeks to use underused land, low-cost financing, and government grants to deliver lower cost rental units. Units delivered as part of the BC Builds program are income tested at the move-in date with certain projects targeting 20% of units rented at 20% below market rates, with the remaining units being targeted at middle income individuals spending no more than 30% of their income on housing. This program is supported by $950 million in provincial funds and access to $2 billion in development financing from the province. In the Budget, the province is contributing an additional $198 million to support the program, including $150 million in operating funding and $48 million in capital funding.[5]

A Growing List of Housing Measures

The measures announced in the Budget follow a flurry of recent legislative activity aimed at moderating the cost of housing. Over the last few years, the province has adopted the following measures:

- Bill 47 (2023), Housing Statutes (Transit-Oriented Areas) Amendment Act, increasing the minimum density required around transit hubs such as sky train stops and bus loops;

- Bill 44 (2023), Housing Statutes (Residential Development) Amendment Act, requiring local governments to up-zone single family properties to allow for a minimum of 2 to 6 units per single family property;

- Bill 22 (2023), Short-Term Rental Accommodations Act, prohibiting self-contained suites from being rented out as short-term accommodations;

- Bill 10 (2023), Budget Measures Implementation Act, providing a $400 a year income tested tax rebate to renters;

- Bill 44 (2022), Building and Strata Statutes Amendment Act, eliminating a strata council’s ability to pass certain age and rental restrictions;

- Bill 43 (2022), Housing Supply Act, establishing housing targets for municipalities; and

- Home Buyer Rescission Period Regulation (2022), providing a three-day rescission period for purchasers of residential real estate.

These recent measures follow significant legislative efforts introduced in previous sessions of the legislature, including:

- the increase of the property transfer tax on high-value real estate;

- the introduction of a foreign buyer’s tax;

- the introduction and expansion of a provincial speculation and vacancy tax;

- an increase in school taxes levied against high value residential real estate; and

- the establishment of a beneficial ownership transparency registry.

British Columbia continues to enjoy a reputation as a highly desirable place to live for existing residents and newcomers alike. The desirability, however, continues to cause affordability issues for residents. High interest rates, labour costs, and a complex regulatory environment continue to frustrate the province’s goal of improving housing affordability. With the 2024 British Columbia Budget, the government is seeking to provide some targeted relief and curtail property transfers that might drive up housing prices.

[1] https://www.bcbudget.gov.bc.ca/2024/pdf/2024_Budget_and_Fiscal_Plan.pdf

[2] Budget, page 66

[3] Budget, page 70.

[4] Budget, page 71.

[5] Budget, page 9.

Stay Connected

All form fields are required "*"